BY PHIL SHETSEN

Meet the Jones family, first-generation business owners navigating growth, complexity, and long-term planning in real time. Each phase captures a snapshot of where the family stands at that moment: their balance sheet, their concerns, and the planning decisions in front of them. As the business grows, so do the stakes. Concerns shift and options narrow or expand depending on what was handled earlier.

In this four-part series, we’ll examine the family’s finances, including their business and portfolio, and offer some tweaks along the way. Part 1 begins in the early stages, when the business is working and momentum is strong, but the long-term plan is still taking shape.

The Early Stages: When the Business Is Humming Along, But the Plan Is Still Forming

At 46, Robert Jones is in the thick of it. His business, Jones Transportation, is growing. Revenue is strong, cash flow is steady—the company is doing what it’s supposed to do. Most days, Robert’s attention is exactly where it needs to be: on operations, clients, employees, and the next opportunity.

At home, life is full. His wife Diana is a full-time nurse and helps with the business on the bookkeeping side. One child is in college while the other two are still minors living at home. The days move fast, and the years feel even faster.

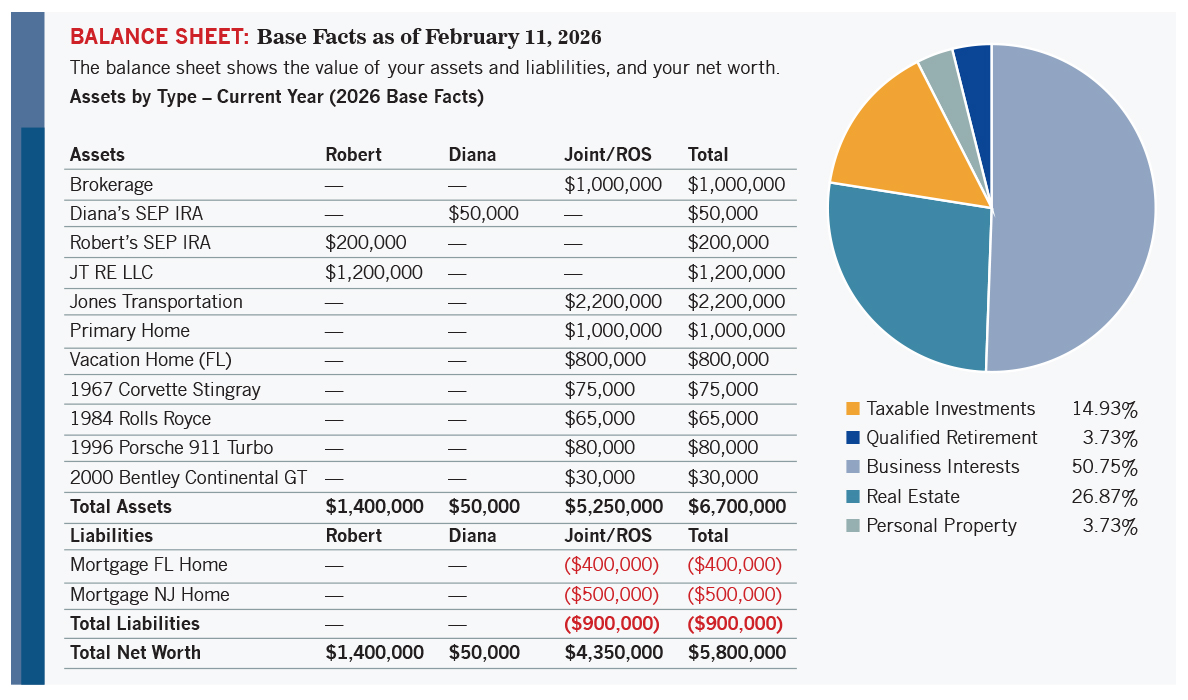

The family’s balance sheet:

From the outside, things look good ... and they are. But this phase has a quiet tension that’s easy to miss.

From the outside, things look good ... and they are. But this phase has a quiet tension that’s easy to miss.

Where the Family Stands

The business is the engine, and it generates roughly $9 million in revenue with about $900,000 in EBITDA. It’s valued around $2.7 million, with about $1 million in assets and $500,000 in debt. The real estate used by the business sits in a separate LLC and is worth another $1.5 million.

Personally, Robert and Diana own a primary residence in New Jersey and a vacation home in Florida, both with mortgages. They’ve built a $1 million non-qualified investment portfolio. Retirement savings exist, but they’re modest at roughly $250,000. There’s also a car collection Robert has built over time, fully paid off.

Nothing here is unusual, but what’s missing is coordination.

The Questions That Haven’t Been Asked Yet

At this stage, the Jones family isn’t worried about legacy or estate taxes. Their estate is valued at about $7.6 million. Instead, the concerns are practical and near-term:

❱ Can the business keep growing without taking on the wrong kind of risk?

❱ Are taxes just the price of success, or could they be managed more intentionally?

❱ If something happened to Robert tomorrow, would the business and the household keep running without disruption?

These are the questions that always sit in the background.

At this stage, planning should begin by establishing a formal spending strategy that clearly separates fixed expenses from variable expenses and ties both to long-term goals. In Robert’s case, that means understanding that the household is running at roughly $20,000 per month—$16,000 fixed and $4,000 variable—and ensuring business compensation supports that.

At this stage, planning should begin by establishing a formal spending strategy that clearly separates fixed expenses from variable expenses and ties both to long-term goals. In Robert’s case, that means understanding that the household is running at roughly $20,000 per month—$16,000 fixed and $4,000 variable—and ensuring business compensation supports that.

The Blind Spot of Early Success

This initial phase can create a false sense of flexibility. The business throws off cash, so there are savings but without a clear structure. Retirement contributions are made, but not in a way that reflects income or long-term needs. Emergency reserves exist, but they’re not clearly defined at either the household or business level.

A defined emergency reserve should be established—both personally and inside the business—before expansion or acquisition is considered. That means setting aside approximately $144,000 in high-yield savings to cover six to nine months of core household expenses.

The business is still structured as an LLC, even though income has reached a level where that choice increases tax exposure. Compensation decisions are made for convenience, not strategy.

At this income level, evaluating an S-Corporation election becomes critical to reduce self-employment taxes. That shift also requires restructuring compensation from owner draws to a reasonable W-2 salary, potentially including Diana on payroll for legitimate business work.

Quarterly profitability and tax review meetings should be formalized to evaluate operating reserves, projected liabilities, and distribution strategy rather than waiting until year-end.

Overall, none of this causes immediate pain—but that’s why it’s easy to overlook.

What Planning Looks Like at This Stage

Early planning is about building a base that won’t crack later. For the Jones family, this is the moment to slow things down and ask some necessary questions: How much income is needed to support today versus tomorrow? Which dollars should be spent, and which should be saved? How exposed is the family if the business hits turbulence or Robert can’t work? Is the business structure still serving them?

Addressing these questions leads to foundational moves:

❱ Implementing a structured savings plan with specific buckets for retirement, college funding, and mid-term goals.

❱ Maximizing tax-advantaged accounts, including building a 401(k) for the business, contributing up to allowable employee deferrals, and evaluating profit-sharing options

❱ For a married couple, that could mean creating up to $23,500 in annual deductions per spouse through qualified retirement contributions, dramatically improving tax efficiency

❱ Opening and funding 529 plans for the younger children and evaluating UGMA accounts where appropriate

❱ Reviewing insurance coverage to address immediate capital needs including debt payoff (approximately $900,000), projected college costs (roughly $650,000), and income replacement needs to protect the family’s $20,000 monthly lifestyle

❱ Updating or drafting core protection documents such as powers of attorney, medical directives, and basic estate documents, even if estate taxes are not currently a concern

Why Early Planning Sets the Tone

This is the time to form healthy habits and where strong structures are built. As the Jones family moves forward, the business will grow, assets will diversify, and family dynamics will change. Each new phase will bring more complexity and fewer clean choices.

Planning early doesn’t prevent future challenges, but it does make them more manageable.

In part two of this case study, success accelerates and the margin for slow decisions starts to disappear.

Tune in next time. [CD0326]

Phil Shetsen is the President of Bona Vita Benefits. He can be reached at